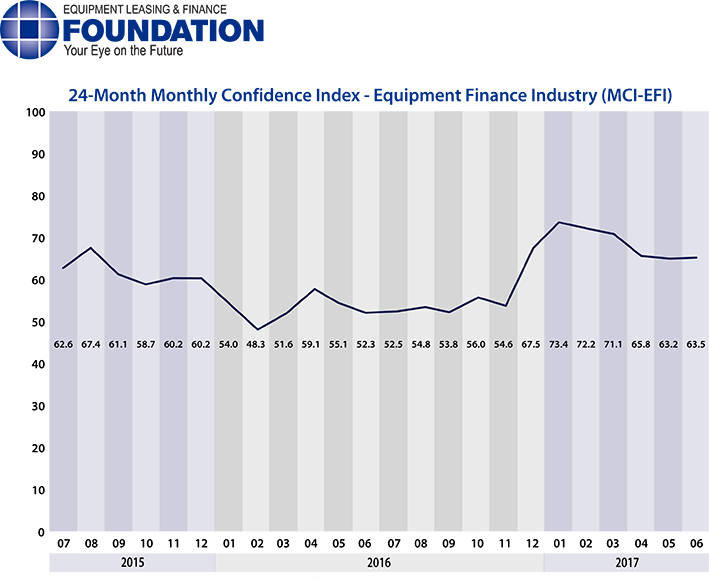

The Equipment Leasing & Finance Foundation (the Foundation) releases the June 2017 Monthly Confidence Index for the Equipment Finance Industry (MCI-EFI) today. Designed to collect leadership data, the index reports a qualitative assessment of both the prevailing business conditions and expectations for the future as reported by key executives from the $1 trillion equipment finance sector. Overall, confidence in the equipment finance market remained steady in June at 63.5, relatively unchanged from the May index of 63.2.

When asked about the outlook for the future, MCI-EFI survey respondent Valerie Hayes Jester, President, Brandywine Capital Associates, said, “Our business volume remains steady, but it is not on pace to exceed last year’s numbers. We see larger companies moving ahead and making capital investments but the smaller businesses seem to be more worried about the instabilities in Washington. The optimism of Wall Street is not shared by Main Street. Portfolio performance remains strong but certainty needs to return to the environment of the average small business owner before investment of a growing scale returns.”

June 2017 Survey Results

The overall MCI-EFI is 63.5, steady with the May index of 63.2.

- When asked to assess their business conditions over the next four months, 31% of executives responding said they believe business conditions will improve over the next four months, an increase from 22.6% in May. 69% of respondents believe business conditions will remain the same over the next four months, a decrease from 71% in May. None believe business conditions will worsen, a decrease from 6.5% the previous month.

- 17.2% of survey respondents believe demand for leases and loans to fund capital expenditures (capex) will increase over the next four months, a decrease from 38.7% in May. 82.8% believe demand will “remain the same” during the same four-month time period, up from 54.8% the previous month. None believe demand will decline, down from 6.5% who believed so in May.

- 13.8% of the respondents expect more access to capital to fund equipment acquisitions over the next four months, up from 12.9% in May. 86.2% of executives indicate they expect the “same” access to capital to fund business, up from 83.9% last month. None expect “less” access to capital, a decrease from 3.2% last month.

- When asked, 41.1% of the executives report they expect to hire more employees over the next four months, a decrease from 45.2% in May. 51.6% expect no change in headcount over the next four months, unchanged from last month. None expect to hire fewer employees, down from 3.2% in May.

- None of the leadership evaluate the current U.S. economy as “excellent,” unchanged from last month. 100% of the leadership evaluate the current U.S. economy as “fair,” and none evaluate it as “poor,” both also unchanged from May.

- 41.4% of the survey respondents believe that U.S. economic conditions will get “better” over the next six months, a slight decrease from 41.9% in May. 51.7% of survey respondents indicate they believe the U.S. economy will “stay the same” over the next six months, unchanged from the previous month. 6.9% believe economic conditions in the U.S. will worsen over the next six months, up slightly from 6.5% who believed so last month.

- In June, 48.3% of respondents indicate they believe their company will increase spending on business development activities during the next six months, an increase from 45.2% in May. 51.7% believe there will be “no change” in business development spending, unchanged from the previous month. None believe there will be a decrease in spending, down from 3.2% last month.

Survey Demographics

Market Segment:

- Bank: 65.5%

- Captive: 10.3%

- Financial Services: 0.0%

- Independent: 24.1%

- Other: 0.0%

Market Segments Based on Transaction Size of New Business Volume

- Large-Ticket (New Business Volume Avg. Transaction Size Over $5 Million): 17.2%

- Middle-Ticket (New Business Volume Avg. Transaction Size of $250,000 – $5 Million): 44.8%

- Small-Ticket (New Business Volume Avg. Transaction Size of $25,000 – $249,999): 37.9%

- Micro-Ticket (New Business Volume Avg. Transaction Less Than $25,000): 0.0%

Organization Size:

- Under $50 Million: 6.9%

- $50 Million – $250 Million: 10.3%

- $250 Million – $1 Billion: 31.0%

- Over $1 Billion: 51.7%

June 2017 Survey Comments from Industry Executive Leadership

Depending on the market segment they represent, executives have differing points of view on the current and future outlook for the industry.

Bank, Middle Ticket

“The cash grain sector of the agriculture industry continues to experience a rebalancing resulting in pull back in new capital investment. Other agriculture sectors are also impacted as they work through down cycles. Some sectors—swine, poultry, nuts and wine producers—are engaged in growth activities resulting in finance opportunities.” Michael Romanowski, President, Farm Credit Leasing Services Corporation

Bank, Small Ticket

The fundamental health of the business community and consumer participation are positives for the near term. The risk to the economy is the political climate and uncertainty it is creating in various industries dependent upon trade, tourism, and policies that support growth.” Paul Menzel, CLFP, President and CEO, Financial Pacific Leasing, Inc., an Umpqua Bank Company

Bank, Large Ticket

“The economy appears to be moving along at a good pace. Uncertainty in Washington and lack of momentum around tax policy could impact capital spending in the second half of the year.” Thomas Partridge, President, Fifth Third Equipment Finance

Back to Top