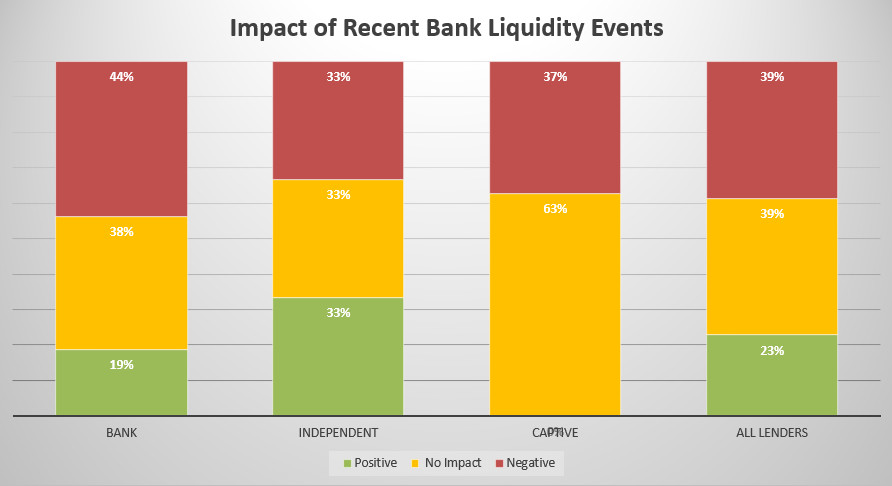

Impact

When asked how they expect to be impacted by the recent liquidity crisis 44% of Banks reported they expected a negative impact, 63% of Captives expected no impact. Independents were equally split on how they expected to be impacted.

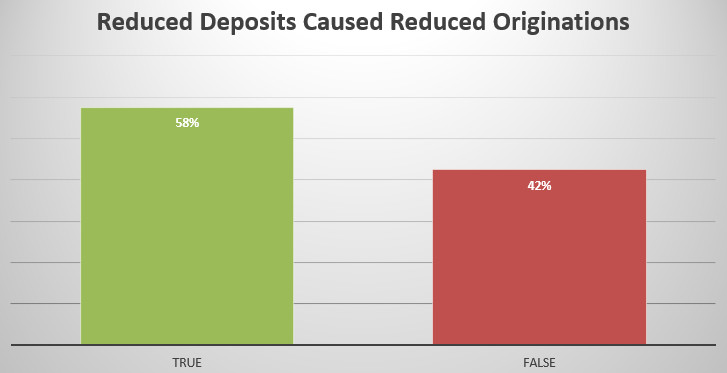

Deposits

When asked if changes in deposit level would reduce new transaction origination and funding activity, 58% of Banks of believed they would.

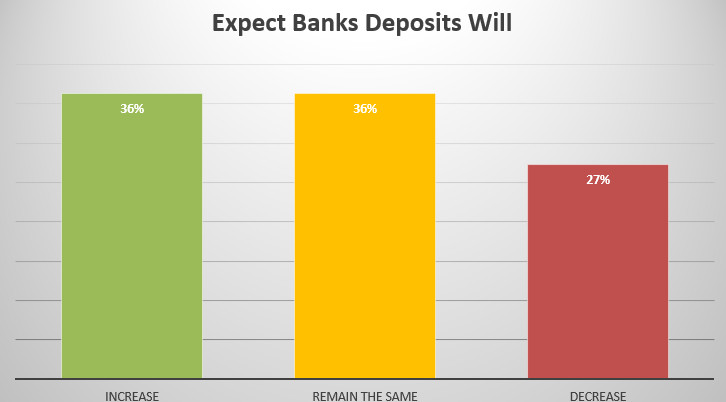

An equal amount of respondents expect deposits at their Banks to increase or remain the same.

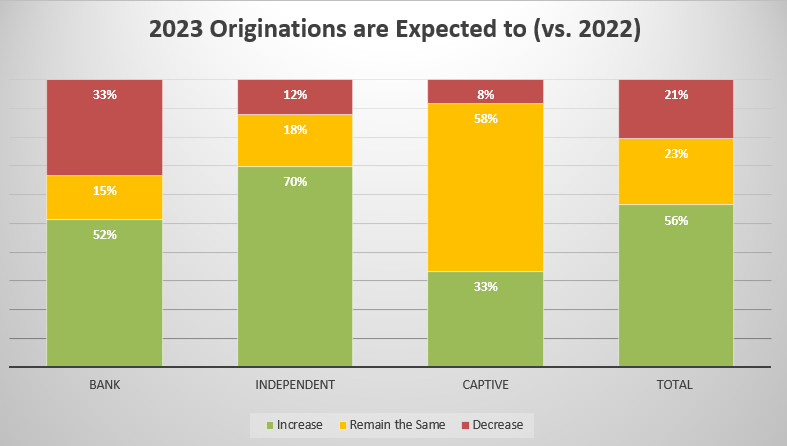

Origination Volume Short & Long Term Impact

Despite these pressures, the majority of lenders expect originations volume to increase in 2023. There was a barbell among Bank lenders, however, with 52% expecting an increase, 33% a decrease, and only 15% expecting volume to remain the same.

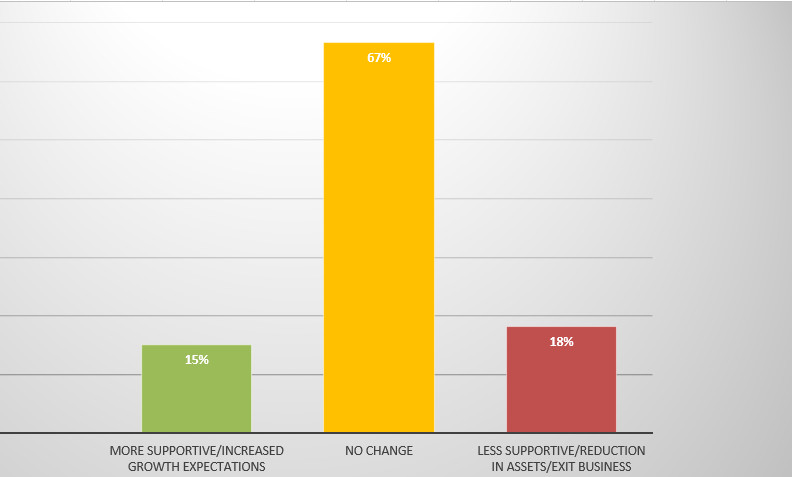

When bank owned leasing companies were asked what about expectations of business growth with respect to the equipment finance products, 67% reported they expected no change as result of the liquidity crisis.

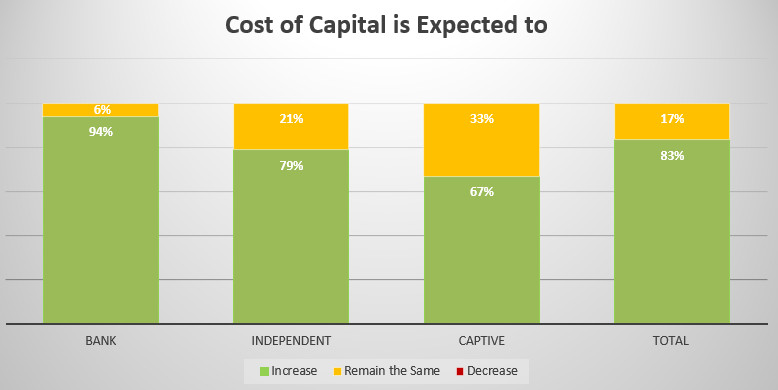

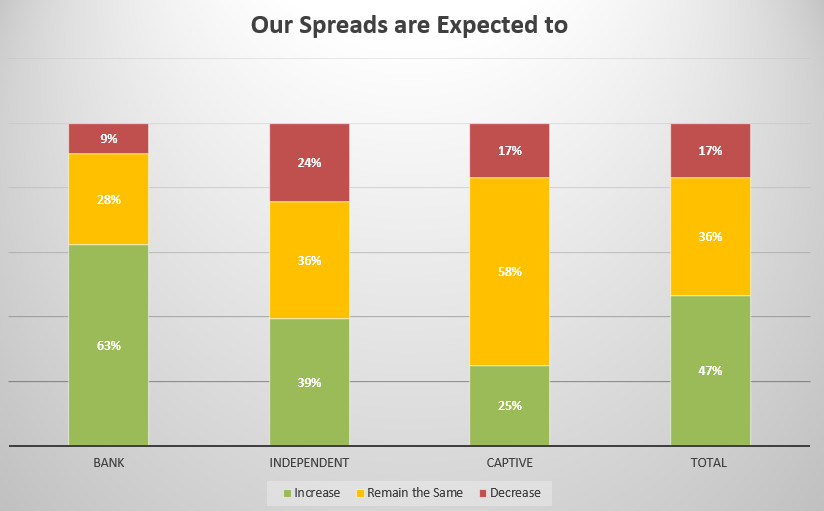

Cost of Capital and Spreads

All types of institutions expect their cost of capital to increase.

While 63% of Banks and 39% of Independents believe their margin requirement or credit spread will increase, Captives were more likely to respond that they will remain the same.

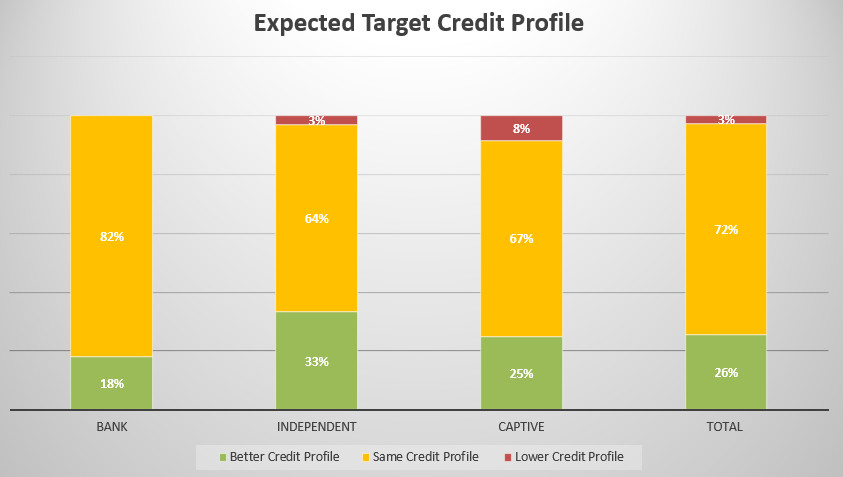

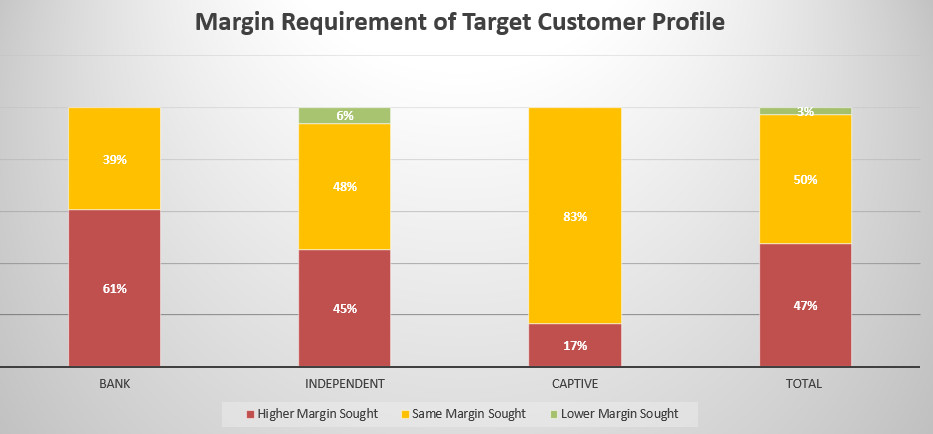

Credit Profiles and Margin Requirements

When asked if they expect the credit profile of their target customer to change, the majority of respondents reported they would be seeking the same credit profile.

When asked if they expect margin requirements of their target customer to change, 83% of Captives and 48% of Independents said they would seek the same margin while 61% of Banks said they would seek a higher margin.

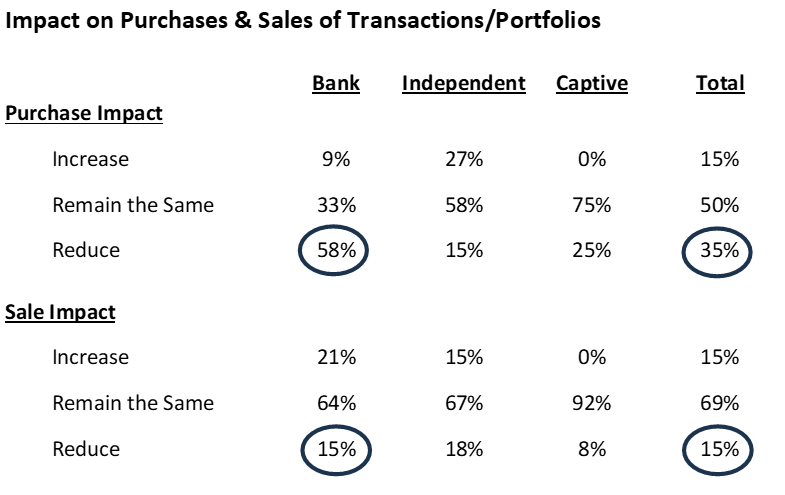

Impact on Purchases & Sales of Transactions/Portfolios

Most Banks, 58% said they would Reduce their Purchasing, but only 15% said they would Reduce their Selling, likely foretelling a market imbalance with more sellers than buyers. The difference was less extreme when all lender types are counted, with 35% saying they would Reduce Purchasing and only 15% saying they would Reduce Selling, but the difference is still material.

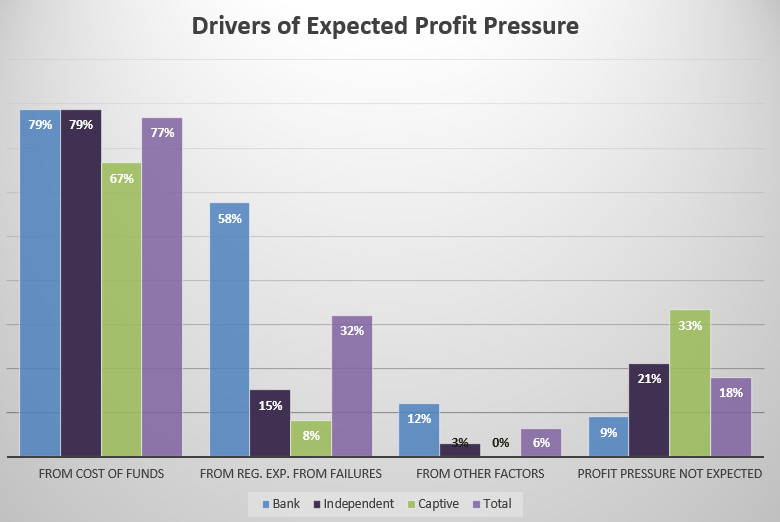

Profit Pressure and Purchase Impact

When asked if they expected profit pressure or erosion to to occur, the majority of respondents across all company types said pressure was most likely to come from cost of funds.

The majority of respondents across all company types believe their purchase impact will not be affected by liquidity stress on capital markets activity.

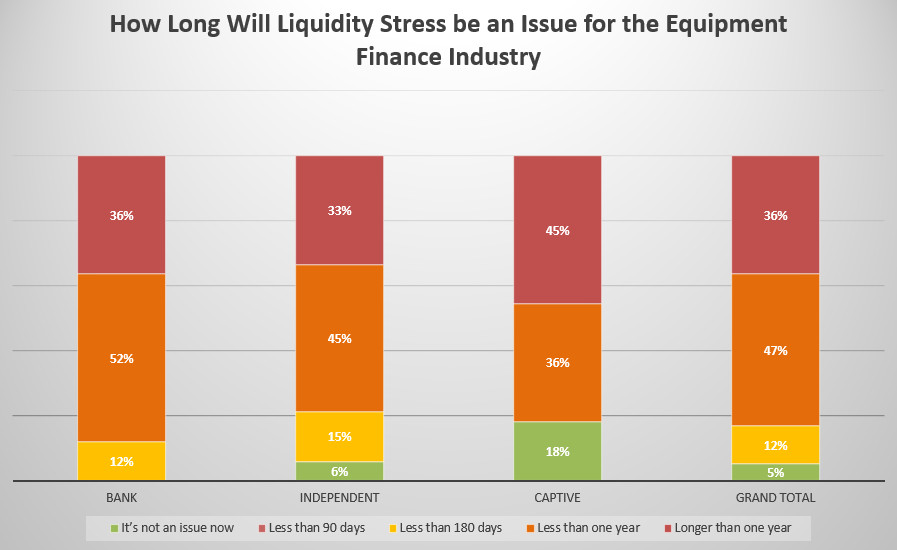

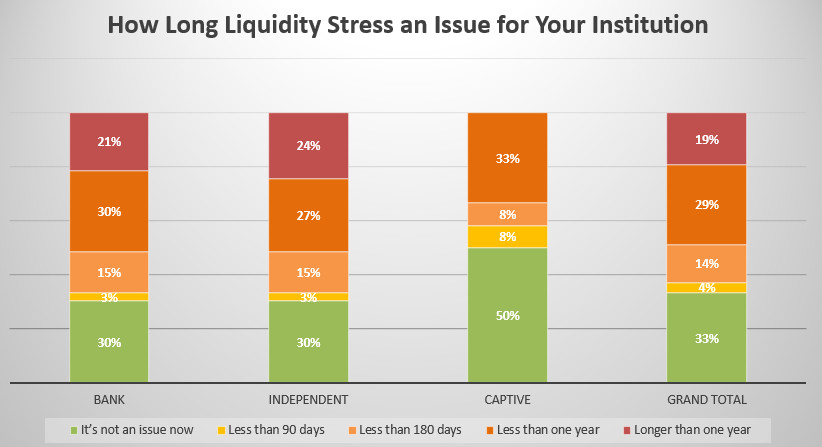

How Long Will Liquidity Stress be an Issue

When asked how long they believed liquidity stress will remain as an issue for the equipment finance industry, 83% say it will be an issue for at least half a year, and over a third say more than a year.

One-third say it's not an issue for their institution now, but 95% (and 100% of Banks) say it is an issue now for the industry.

Acknowledgments

We would like to acknowledge the support of the Equipment Leasing & Finance Foundation Research Committee volunteers who contributed to this survey and data analysis, including Chris Enbom, Valerie Gerard, Chris Kelley, Eli Sethre, Will Tefft, Tom Ware and Donna Yanuzzi.