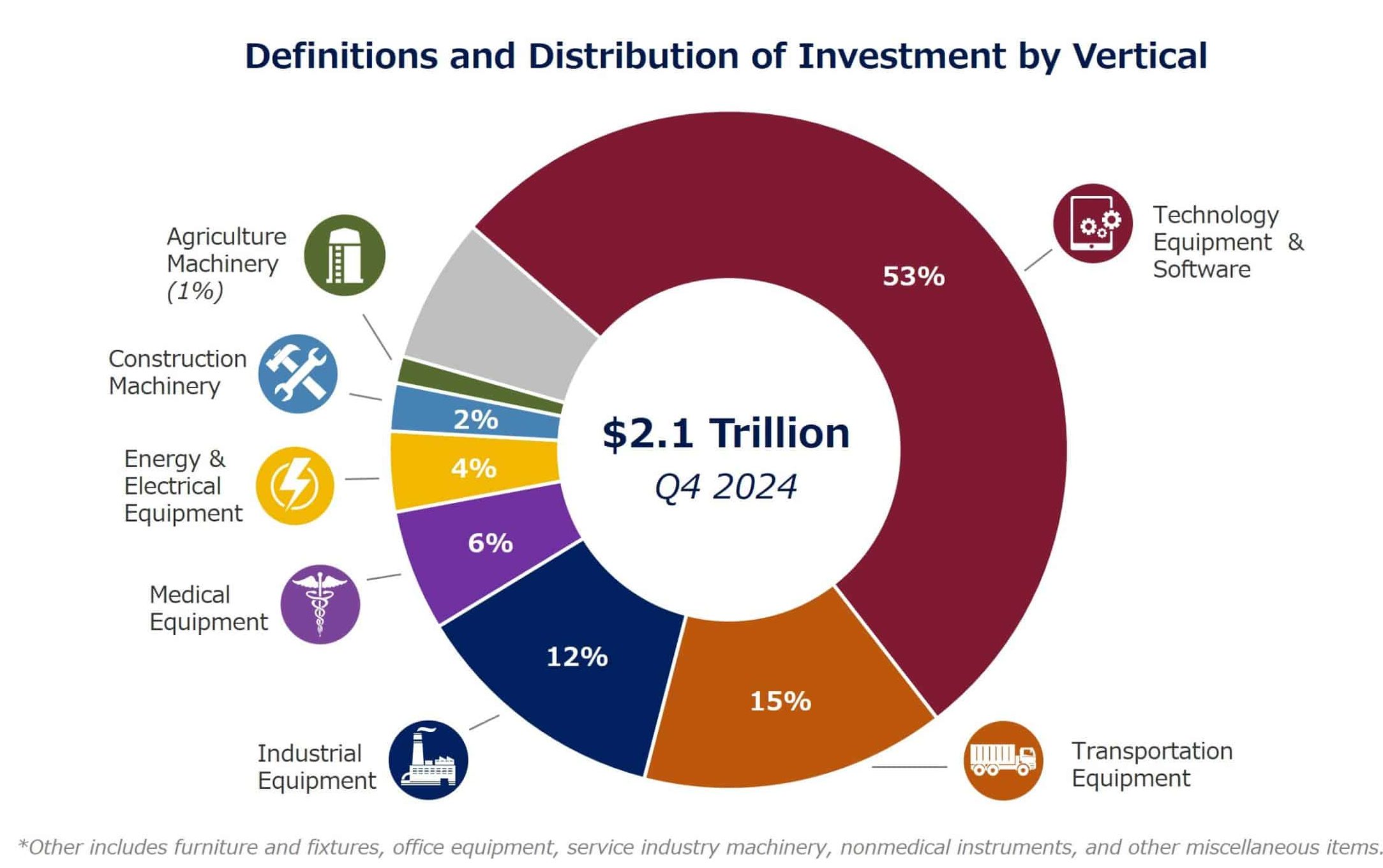

The Foundation consolidated several equipment verticals while also incorporating new types of equipment that have not previously been tracked. Specifically, the number of equipment verticals has been condensed from 12 to 7, including Agriculture, Construction, Energy & Electrical, Industrial, Medical, Technology, and Transportation. Collectively, these verticals account for over 90% of U.S. equipment and software investment.