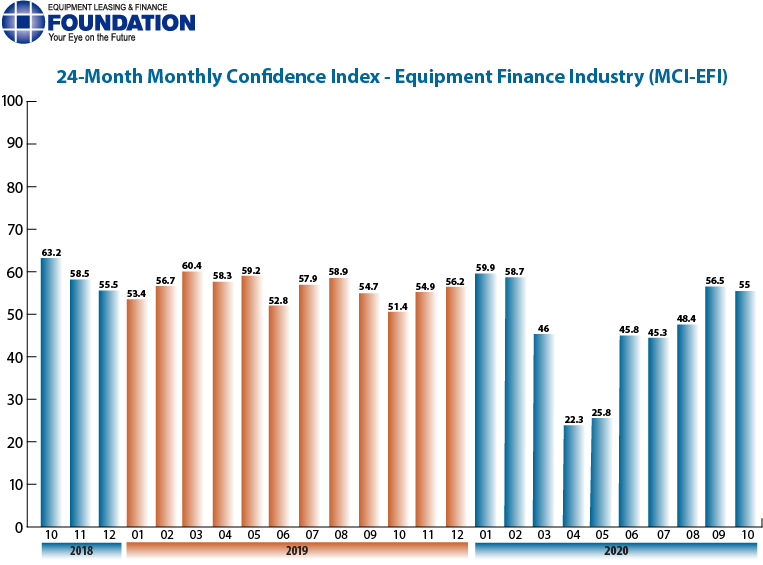

The Equipment Leasing & Finance Foundation (the Foundation) releases the October 2020 Monthly Confidence Index for the Equipment Finance Industry (MCI-EFI) today. The index reports a qualitative assessment of both the prevailing business conditions and expectations for the future as reported by key executives from the $900 billion equipment finance sector. Overall, confidence in the equipment finance market is 55.0, easing from the September index of 56.5 and steady with pre-COVID index levels.

The Foundation also releases highlights of the COVID-19 Impact Survey of the Equipment Finance Industry, a monthly survey of industry leaders designed to track the impact of the coronavirus pandemic on the equipment finance industry.

When asked about the outlook for the future, MCI-EFI survey respondent Bruce J. Winter, President, FSG Capital, Inc., said, “It’s now obvious that the economic fallout from this pandemic will continue for the foreseeable future and there will be no quick return to pre-COVID 19 economic metrics. While many of our clients have adapted to a new normal, others have spent their government stimulus and are at risk of closure without additional support. The resiliency of the equipment finance industry is without doubt, but as with other cycles, there will be winners and losers. In this cycle, those lucky enough to have little or no exposure to threatened industries will be the winners, while those with too much exposure to these same segments have no choice but to deal with significant stress.”

October 2020 Survey Results

The overall MCI-EFI is 55.0, a decrease from the September index of 56.5.

- When asked to assess their business conditions over the next four months, 29.6% of executives responding said they believe business conditions will improve over the next four months, down from 35.7% in September. 51.9% believe business conditions will remain the same over the next four months, an increase from 46.4% the previous month. 18.5% believe business conditions will worsen, an increase from 17.9% in September.

- 22.2% of the survey respondents believe demand for leases and loans to fund capital expenditures (capex) will increase over the next four months, down from 28.6% in September. 66.7% believe demand will “remain the same” during the same four-month time period, an increase from 64.3% the previous month. 11.1% believe demand will decline, an increase from 7.1% in September.

- 33.3% of the respondents expect more access to capital to fund equipment acquisitions over the next four months, up from 17.9% in September. 66.7% of executives indicate they expect the “same” access to capital to fund business, a decrease from 78.6% last month. None expect “less” access to capital, a decrease from 3.6% the previous month.

- When asked, 25.9% of the executives report they expect to hire more employees over the next four months, up from 17.9% in September. 63% expect no change in headcount over the next four months, a decrease from 71.4% last month. 11.1% expect to hire fewer employees, up slightly from 10.7% the previous month.

- None of the leadership evaluate the current U.S. economy as “excellent,” unchanged from the previous month. 55.6% of the leadership evaluate the current U.S. economy as “fair,” up from 46.4% in September. 44.4% evaluate it as “poor,” down from 53.6% last month.

- 25.9% of the survey respondents believe that U.S. economic conditions will get “better” over the next six months, a decrease from 50% in September. 59.3% indicate they believe the U.S. economy will “stay the same” over the next six months, an increase from 39.3% last month. 14.8% believe economic conditions in the U.S. will worsen over the next six months, up from 10.7% the previous month.

- In October, 22.2% of respondents indicate they believe their company will increase spending on business development activities during the next six months, a decrease from 28.6% last month. 70.4% believe there will be “no change” in business development spending, a decrease from 71.4% in September. 7.4% believe there will be a decrease in spending, up from none last month.

October 2020 Survey Comments from Industry Executive Leadership

Bank, Small Ticket

“Wintrust Specialty Finance has experienced strong originations, yields and portfolio performance in the third quarter. Our application volume has been continuing to grow, and the overall credit quality has been good. While I think the election will affect volume in the fourth quarter of 2020, the market will adapt and continue forward.” David Normandin, CLFP, President and CEO, Wintrust Specialty Finance

Bank, Middle Ticket

“We continue to see opportunities, especially with customers who traditionally use cash for expansion but are presently looking to lock in long-term, low rates.” Michael Romanowski, President, Farm Credit Leasing

“Within each industry we serve, there are pockets of companies that are doing quite well and continue to invest in the future. Many organizations have accelerated investment in digital transformation, upgrading software and workforce mobility.” Alan Sikora, CLFP, CEO, First American Equipment Finance, an RBC / City National Company

Back to Top