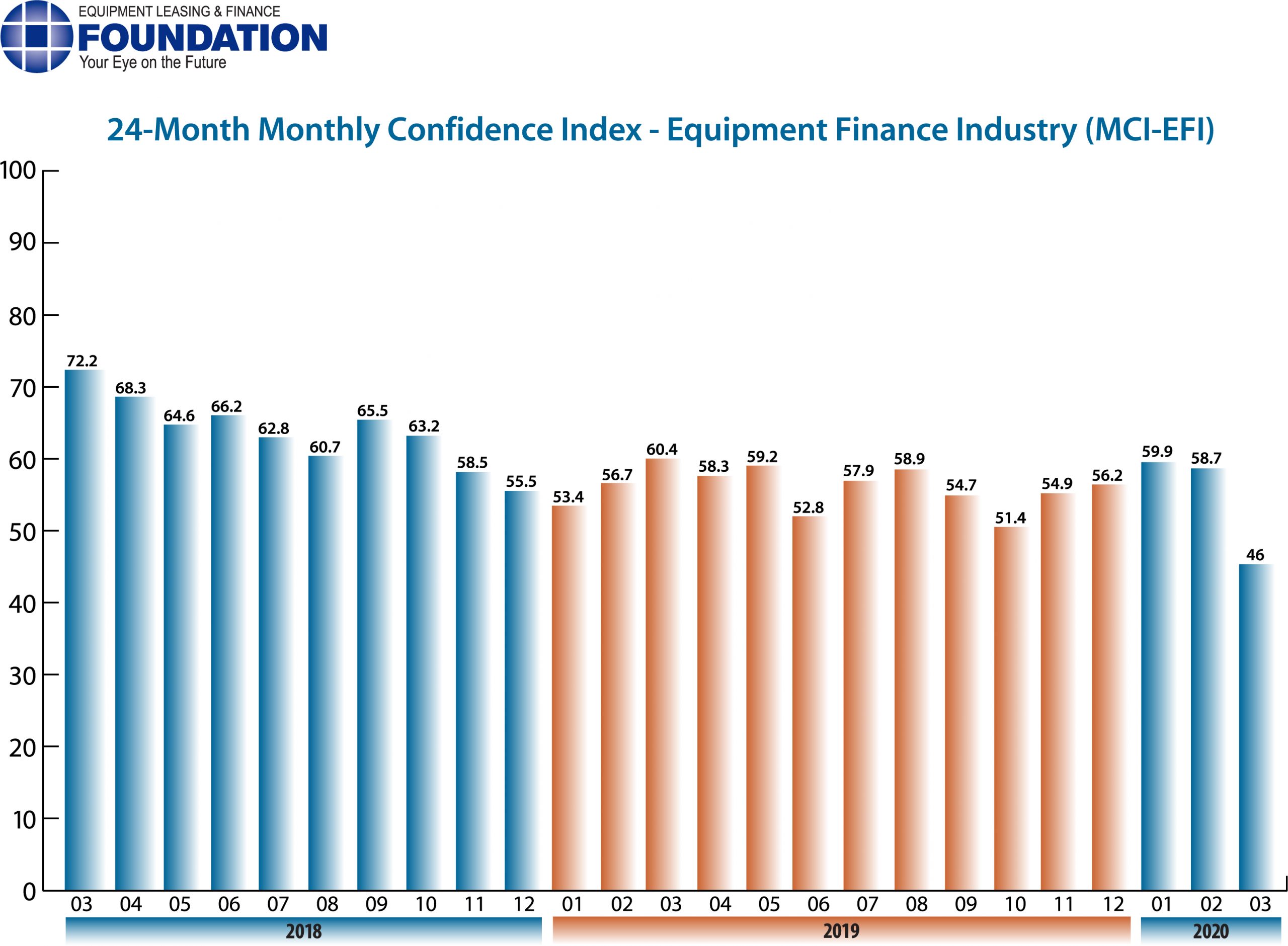

The Equipment Leasing & Finance Foundation (the Foundation) releases the March 2020 Monthly Confidence Index for the Equipment Finance Industry (MCI-EFI) today. Designed to collect leadership data, the index reports a qualitative assessment of both the prevailing business conditions and expectations for the future as reported by key executives from the $900 billion equipment finance sector. Overall, confidence in the equipment finance market in March is 46.0, a decrease from the February index of 58.7.

When asked about the outlook for the future, MCI-EFI survey respondent Valerie Hayes Jester, President, Brandywine Capital Associates, said, “The fundamentals of our economy continue to be strong. The current events in the worldwide markets and the impact of COVID-19 are impacting the very near term. Business demand for equipment finance is always based on the long-term perspectives of the commercial sectors, and I do not believe that pessimism is the predominant emotion in our customer base. 2019 was a strong year and I have no reason to believe that demand will not continue to increase in the future. I did not agree with the Federal Reserve’s action of lowering rates, and I don’t believe that the decrease will have any impact on the equipment acquisition decisions of small businesses.”

March 2020 Survey Results

The overall MCI-EFI is 46.0, a decrease from 58.7 in February.

- When asked to assess their business conditions over the next four months, 3.7% of executives responding said they believe business conditions will improve over the next four months, down from 11.5% in February. 48.2% of respondents believe business conditions will remain the same over the next four months, a decrease from 84.6% the previous month. 48.2% believe business conditions will worsen, an increase from 3.9% in February.

- 3.7% of the survey respondents believe demand for leases and loans to fund capital expenditures (capex) will increase over the next four months, a decrease from 7.7% in February. 59.3% believe demand will “remain the same” during the same four-month time period, a decrease from 88.5% the previous month. 37% believe demand will decline, an increase from 3.9% in February.

- 14.8% of the respondents expect more access to capital to fund equipment acquisitions over the next four months, a decrease from 19.2% in February. 77.8% of executives indicate they expect the “same” access to capital to fund business, an increase from 76.9% last month. 7.4% expect “less” access to capital, an increase from 3.9% the previous month.

- When asked, 29.6% of the executives report they expect to hire more employees over the next four months, a decrease from 30.8% in February. 66.7% expect no change in headcount over the next four months, an increase from 61.5% last month. 3.7% expect to hire fewer employees, down from 7.7% the previous month.

- 18.5% of the leadership evaluate the current U.S. economy as “excellent,” down from 38.5% the previous month. 77.8% of the leadership evaluate the current U.S. economy as “fair,” up from 61.5% in February. 3.7% evaluate it as “poor,” up from none last month.

- 14.8% of the survey respondents believe that U.S. economic conditions will get “better” over the next six months, an increase from 4% in February. 37% indicate they believe the U.S. economy will “stay the same” over the next six months, a decrease from 88% last month. 48.2% believe economic conditions in the U.S. will worsen over the next six months, up from 8% the previous month.

- In March, 22.2% of respondents indicate they believe their company will increase spending on business development activities during the next six months, a decrease from 50% last month. 70.4% believe there will be “no change” in business development spending, up from 42.3% in February. 7.4% believe there will be a decrease in spending, relatively unchanged from 7.7% last month.

Survey Demographics

Market Segment

- Bank 51.8%

- Captive 14.8%

- Financial Services 3.7%

- Independent 25.9%

- Other 3.7%

Market Segments Based on Transaction Size of New Business Volume

- Large-Ticket (New Business Volume Avg. Transaction Size Over $5 Million) 23.1%

- Middle-Ticket (New Business Volume Avg. Transaction Size of $250,000 – $5 Million) 42.3%

- Small-Ticket (New Business Volume Avg. Transaction Size of $25,000 – $249,999) 34.6%

- Micro-Ticket (New Business Volume Avg. Transaction Less Than $25,000) 0.00%

Organization Size

- Under $50 Million 11.1%

- $50 Million – $250 Million 14.8%

- $250 Million – $1 Billion 25.9%

- Over $1 Billion 48.1%

March 2020 Survey Comments from Industry Executive Leadership

Bank, Small Ticket

“I am optimistic about the near future simply based upon the metrics in the business that demonstrate increased application flow, strong approval rates, and consistent pull through.” David Normandin, CLFP, President and CEO, Wintrust Specialty Finance

Bank, Middle Ticket

“Banks and finance companies need to understand the impact that the coronavirus outbreak may have on their portfolios and new business. Manufacturing, shipping, travel, and healthcare are just a few examples of potential affected sectors.” Adam Warner, President, Key Equipment Finance

“We expect moderate growth this year as agribusinesses and producers have curtailed capital investment over the past few years. In many cases, investment needs to be made to replace aging equipment. It is still too early to predict the impacts of coronavirus on our customer base and if it will have an impact on capital investment. Presently, we believe coronavirus will have minimal impact on planned capital investment activities.” Michael Romanowski, President, Farm Credit Leasing

Back to Top