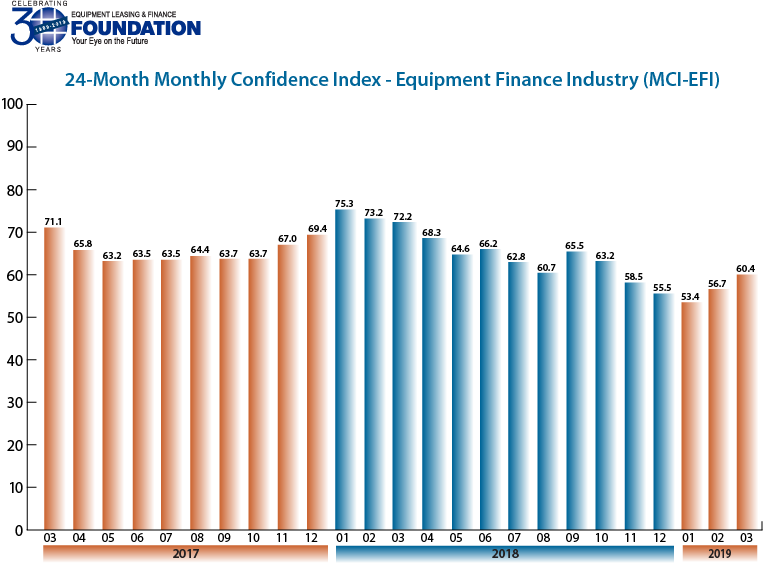

Washington, DC, March 14, 2019 – The Equipment Leasing & Finance Foundation (the Foundation) releases the March 2019 Monthly Confidence Index for the Equipment Finance Industry (MCI-EFI) today. Designed to collect leadership data, the index reports a qualitative assessment of both the prevailing business conditions and expectations for the future as reported by key executives from the $1 trillion equipment finance sector. Overall, confidence in the equipment finance market increased in March for the second consecutive month to 60.4, up from the February index of 56.7.

When asked about the outlook for the future, MCI-EFI survey respondent Harry Kaplun, President, Specialty Finance, Frost Bank, said, “This year will continue to be prosperous as economic indicators are predicting. Business growth is spurred by low interest rates, favorable tax rates and expansion oriented investment.”

March 2019 Survey Results

The overall MCI-EFI is 60.4, an increase from 56.7 in February.

- When asked to assess their business conditions over the next four months, 20% of executives responding said they believe business conditions will improve over the next four months, up from 10% in February. 70% of respondents believe business conditions will remain the same over the next four months, a decrease from 83.3% the previous month. 10% believe business conditions will worsen, up from 6.7% who believed so the previous month.

- 23.3% of survey respondents believe demand for leases and loans to fund capital expenditures (capex) will increase over the next four months, an increase from 13.3% in February. 70% believe demand will “remain the same” during the same four-month time period, a decrease from 83.3% the previous month. 6.7% believe demand will decline, up from 3.3% who believed so in February.

- 13.3% of the respondents expect more access to capital to fund equipment acquisitions over the next four months, down from 20.7% in February. 86.7% of executives indicate they expect the “same” access to capital to fund business, an increase from 79.3% last month. None expect “less” access to capital, unchanged from last month.

- When asked, 46.7% of the executives report they expect to hire more employees over the next four months, an increase from 26.7% in February. 46.7% expect no change in headcount over the next four months, a decrease from 56.7% last month. 6.7% expect to hire fewer employees, down from 16.7% last month.

- 36.7% of the leadership evaluate the current U.S. economy as “excellent,” 63.3% of the leadership evaluate the current U.S. economy as “fair,” and none evaluate it as “poor,” all unchanged for the second consecutive month.

- 6.7% of the survey respondents believe that U.S. economic conditions will get “better” over the next six months, down from 13.3% in February. 80% of survey respondents indicate they believe the U.S. economy will “stay the same” over the next six months, an increase from 70% the previous month. 13.3% believe economic conditions in the U.S. will worsen over the next six months, a decrease from 16.7% in February.

- In March, 33.3% of respondents indicate they believe their company will increase spending on business development activities during the next six months, an increase from 20% last month. 66.7% believe there will be “no change” in business development spending, a decrease from 80% in February. None believe there will be a decrease in spending, unchanged from last month.

Survey Demographics

Market Segment

- Bank 65.5%

- Captive 13.8%

- Financial Services 3.4%

- Independent 17.2%

- Other 0%

Market Segments Based on Transaction Size of New Business Volume

- Large-Ticket (New Business Volume Avg. Transaction Size Over $5 Million) 16.7%

- Middle-Ticket (New Business Volume Avg. Transaction Size of $250,000 – $5 Million) 53.3%

- Small-Ticket (New Business Volume Avg. Transaction Size of $25,000 – $249,999) 30%

- Micro-Ticket (New Business Volume Avg. Transaction Less Than $25,000) 0.00%

Organization Size

- Under $50 Million 6.6%

- $50 Million – $250 Million 13.3%

- $250 Million – $1 Billion 20%

- Over $1 Billion 60%

March 2019 Survey Comments from Industry Executive Leadership

Bank, Small Ticket

“Consolidation in the industry will continue to create opportunity. The overall application volume has remained stable.” David Normandin, CLFP, President and CEO, Wintrust Specialty Finance

Independent, Small Ticket

“I’m optimistic that companies in general have ample cash and access to capital to withstand any softening of demand. I’m concerned about the softening housing market and the negative impact it may have on small business sentiment.” Quentin Cote, CLFP, President, Mintaka Financial, LLC

Bank, Middle Ticket

“Federal government concerns cast a shadow over economic optimism.” Adam Warner, President, Key Equipment Finance

Back to Top