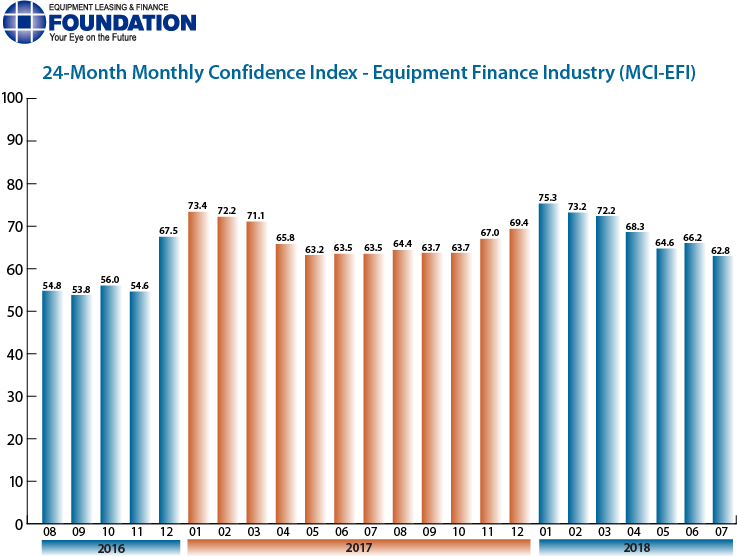

The Equipment Leasing & Finance Foundation (the Foundation) releases the July 2018 Monthly Confidence Index for the Equipment Finance Industry (MCI-EFI) today. Designed to collect leadership data, the index reports a qualitative assessment of both the prevailing business conditions and expectations for the future as reported by key executives from the $1 trillion equipment finance sector. Overall, confidence in the equipment finance market is 62.8 in July, easing from the June index of 66.2.

When asked about the outlook for the future, MCI-EFI survey respondent Michael Romanowski, President, Farm Credit Leasing Services Corporation, said, “Customers continue to digest the changes related to tax reform to determine how best to finance capital investment. Some customers are delaying capital investment until they better understand the impacts related to tariffs.”

Survey Results

The overall MCI-EFI is 62.8 in July, a decrease from 66.2 in June.

- When asked to assess their business conditions over the next four months, 19.4% of executives responding said they believe business conditions will improve over the next four months, a decrease from 33.3% in June. 77.4% of respondents believe business conditions will remain the same over the next four months, an increase from 63.6% the previous month. 3.2% believe business conditions will worsen, relatively unchanged from 3.0% who believed so the previous month.

- 19.4% of survey respondents believe demand for leases and loans to fund capital expenditures (capex) will increase over the next four months, a decrease from 24.2% in June. 77.4% believe demand will “remain the same” during the same four-month time period, an increase from 75.8% the previous month. 3.2% believe demand will decline, up from none who believed so in June.

- 16.1% of the respondents expect more access to capital to fund equipment acquisitions over the next four months, up from 15.2% in June. 83.9% of executives indicate they expect the “same” access to capital to fund business, a decrease from 84.9% last month. None expect “less” access to capital, unchanged from last month.

- When asked, 45.2% of the executives report they expect to hire more employees over the next four months, a decrease from 57.6% in June. 51.6% expect no change in headcount over the next four months, an increase from 42.4% last month. 3.2% expect to hire fewer employees, an increase from none in June.

- 41.9% of the leadership evaluate the current U.S. economy as “excellent,” up from 39.4% last month. 58.1% of the leadership evaluate the current U.S. economy as “fair,” down from 60.6% in June. None evaluate it as “poor,” unchanged from last month.

- 12.9% of the survey respondents believe that U.S. economic conditions will get “better” over the next six months, a decrease from 24.2% in June. 77.4% of survey respondents indicate they believe the U.S. economy will “stay the same” over the next six months, an increase from 69.7% the previous month. 9.7% believe economic conditions in the U.S. will worsen over the next six months, an increase from 6.1% in June.

- In July, 45.2% of respondents indicate they believe their company will increase spending on business development activities during the next six months, an increase from 42.4% in June. 54.8% believe there will be “no change” in business development spending, a decrease from 57.6% the previous month. None believe there will be a decrease in spending, unchanged from last month.

Survey Demographics

Market Segment

- Bank 64.52%

- Captive 9.68%

- Financial Services 0%

- Independent 22.58%

- Other 3.23%

Market Segments Based on Transaction Size of New Business Volume

- Large-Ticket (New Business Volume Avg. Transaction Size Over $5 Million) 19.35%

- Middle-Ticket (New Business Volume Avg. Transaction Size of $250,000 – $5 Million) 51.61%

- Small-Ticket (New Business Volume Avg. Transaction Size of $25,000 – $249,999) 29.03%

- Micro-Ticket (New Business Volume Avg. Transaction Less Than $25,000) 0.00%

Organization Size

- Under $50 Million 9.68%

- $50 Million – $250 Million 9.68%

- $250 Million – $1 Billion 25.81%

- Over $1 Billion 54.84%

Survey Comments from Industry Executive Leadership

Independent, Small Ticket

“Demand for new and used equipment remains strong so applications are up, and we are seeing some better quality so approvals are up, too. All of this is growing our originations.” David T. Schaefer, CEO, Mintaka Financial, LLC

“Businesses continue to invest in equipment and financing those purchases. The manic nature of the stock markets and our government leadership seems to be having minimal impact on the decisions of our small business customers. It will be an interesting second half of the year as we observe expansion trends among our customers.” Valerie Hayes Jester, President, Brandywine Capital Associates

Bank, Middle Ticket

“Times are good in the U.S. There are no pending problems that can have a significant economic effect.” Harry Kaplun, President, Specialty Finance, Frost Bank

Back to Top