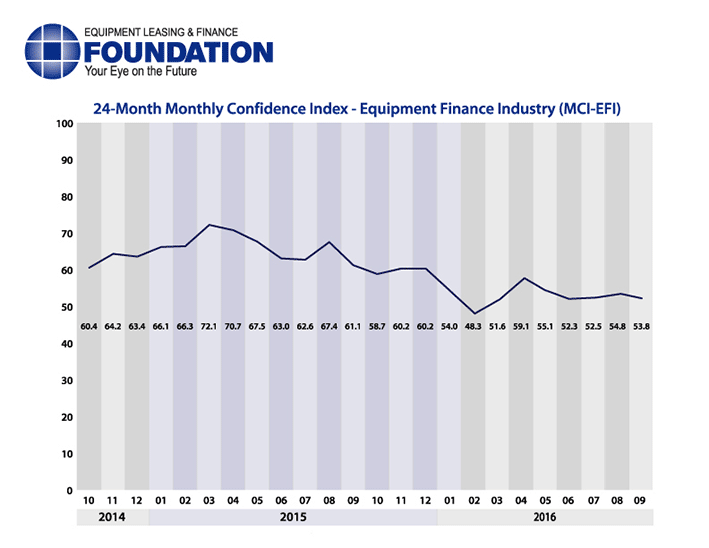

The Equipment Leasing & Finance Foundation (the Foundation) releases the September 2016 Monthly Confidence Index for the Equipment Finance Industry (MCI-EFI) today. Designed to collect leadership data, the index reports a qualitative assessment of both the prevailing business conditions and expectations for the future as reported by key executives from the $1 trillion equipment finance sector. Overall, confidence in the equipment finance market is 53.8, a decrease from the August index of 54.8 as equipment finance executives cite customers’ concerns over the November election.

When asked about the outlook for the future, MCI-EFI survey respondent Thomas Jaschik, President, BB&T Equipment Finance, said, “It appears U.S. companies have put their plans for growth on hold pending the outcome of the presidential election. Capital investment levels continue at diminished levels. As such, the equipment finance industry will experience a reduction in new business volumes as compared to the last several years.”

September 2016 Survey Results

The overall MCI-EFI is 53.8, a decrease from the August index of 54.8.

- When asked to assess their business conditions over the next four months, 18.8% of executives responding said they believe business conditions will improve over the next four months, an increase from 10.0% in August. 62.5% of respondents believe business conditions will remain the same over the next four months, a decrease from 80.0% in August. 18.8% believe business conditions will worsen, an increase from 10.0% the previous month.

- 28.1% of survey respondents believe demand for leases and loans to fund capital expenditures (capex) will increase over the next four months, an increase from 13.3% in August. 53.1% believe demand will “remain the same” during the same four-month time period, down from 70.0% the previous month. 18.8% believe demand will decline, an increase from 16.7% who believed so in August.

- None of the respondents expect more access to capital to fund equipment acquisitions over the next four months, a decrease from 13.3% in August. 96.9% of executives indicate they expect the “same” access to capital to fund business, an increase from 80.0% the previous month. 3.1% expect “less” access to capital, a decrease from 6.7% last month.

- When asked, 21.9% of the executives report they expect to hire more employees over the next four months, a decrease from 40.0% in August. 71.9% expect no change in headcount over the next four months, an increase from 50.0% last month. 6.3% expect to hire fewer employees, down from 10.0% in August.

- None of the leadership evaluate the current U.S. economy as “excellent,” unchanged from last month. 100.0% of the leadership evaluate the current U.S. economy as “fair,” an increase from 90.0% last month. None evaluate it as “poor,” a decrease from 10.0% in August.

- 6.3% of the survey respondents believe that U.S. economic conditions will get “better” over the next six months, an increase from none in August. 75.0% of survey respondents indicate they believe the U.S. economy will “stay the same” over the next six months, a decrease from 96.7% the previous month. 18.8% believe economic conditions in the U.S. will worsen over the next six months, an increase from 3.3% who believed so last month.

- In September, 40.6% of respondents indicate they believe their company will increase spending on business development activities during the next six months, relatively unchanged from 40.0% in August. 53.1% believe there will be “no change” in business development spending, a decrease from 60.0% the previous month. 6.3% believe there will be a decrease in spending, an increase from none who believed so last month.

Survey Demographics

Market Segment:

- Bank: 66.7%

- Captive: 3.3%

- Financial Services: 3.3%

- Independent: 26.7%

- Other: 0.0%

Market Segments Based on Transaction Size of New Business Volume

- Large-Ticket (New Business Volume Avg. Transaction Size Over $5 Million): 20.0%

- Middle-Ticket (New Business Volume Avg. Transaction Size of $250,000 – $5 Million): 36.7%

- Small-Ticket (New Business Volume Avg. Transaction Size of $25,000 – $249,999): 43.3

- Micro-Ticket (New Business Volume Avg. Transaction Less Than $25,000): 0.0%

Organization Size (Based on Annual New Business Volume for Fiscal Year 2010):

- Under $50 Million: 6.7%

- $50 Million – $250 Million: 13.3%

- $250 Million – $1 Billion: 33.3%

- Over $1 Billion: 46.7%

September 2016 Survey Comments from Industry Executive Leadership

Depending on the market segment they represent, executives have differing points of view on the current and future outlook for the industry.

Independent, Small Ticket

“The industry remains strong and dynamic. My concerns in the near team are for inconsistent demand levels in the small ticket marketplace caused mostly by anxiety about the presidential election, hostile world events, and a somewhat volatile stock market. We have seen many transactions placed “on hold” by small and midsize business owners due to lack of confidence. I would have expected that more than eight years past the ‘Great Recession’ we would not be dealing with a manic equipment acquisition pattern.” Valerie Hayes Jester, President, Brandywine Capital Associates

Bank, Small Ticket

“Financial stress increasing in small business is producing increased delinquency and defaults. The U.S. economy is the best place to be, although under stress.” David Normandin, Managing Director, Commercial Finance Group, Banc of California

Bank, Middle Ticket

“Is it good or is it bad? I think neither. In general the industry is motoring along at a steady pace. Industries needing capital for expansion are few and most users of equipment financing are purchasing for replacement or efficiency reasons. Economic and political uncertainties are factors that will take months to understand, thus continuing to suppress capital spending.” Harry Kaplun, President, Specialty Finance, Frost Bank

Independent, Middle Ticket

“There seems to be a slowdown of equipment acquisitions in the smaller ticket market place, especially in truck transportation, both Class 8 and some medium duty. Not sure if it is temporary or a precursor of something else.” William H. Besgen, Senior Advisor, Vice Chairman Emeritus, Hitachi Capital America Corp.

Bank, Large Ticket

“I am concerned about how companies are responding to the election cycle. A rate increase could have a negative impact on exchange rates, which will impact those clients exporting.” Thomas Partridge, President, Fifth Third Equipment Finance

Back to Top