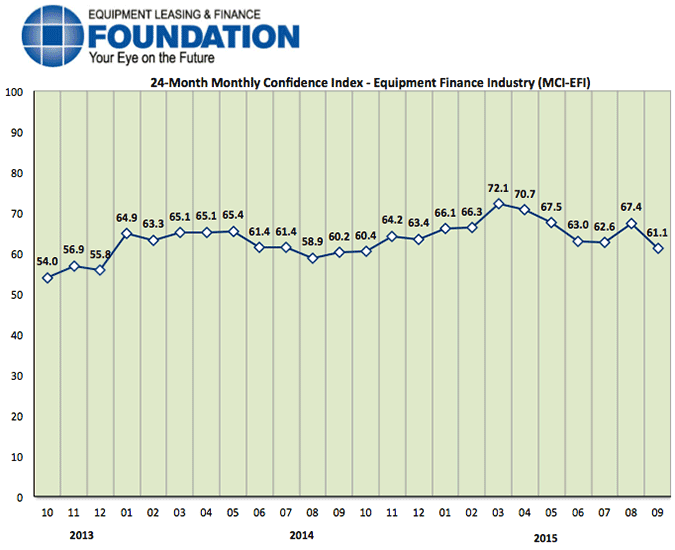

The Equipment Leasing & Finance Foundation (the Foundation) releases the September 2015 Monthly Confidence Index for the Equipment Finance Industry (MCI-EFI) today. Designed to collect leadership data, the index reports a qualitative assessment of both the prevailing business conditions and expectations for the future as reported by key executives from the $903 billion equipment finance sector. Overall, confidence in the equipment finance market is 61.1, easing from the sharp rise in the August index of 67.4.

When asked about the outlook for the future, MCI-EFI survey respondent Thomas Jaschik, President, BB&T Equipment Finance, said, “An increase in interest rates may help to spur activity in the equipment finance sector. Rising costs are always an impetus for taking action now vs. later. Rising interest rates could be the catalyst to push companies to act now with respect to capital equipment acquisitions. This could create tremendous opportunities within the equipment finance market.”

September 2015 Survey Results

The overall MCI-EFI is 61.1, easing from the August index of 67.4.

- When asked to assess their business conditions over the next four months, 22.2% of executives responding said they believe business conditions will improve over the next four months, a decrease from 36.4% in August. 70.4% of respondents believe business conditions will remain the same over the next four months, an increase from 63.6% in August. 7.4% believe business conditions will worsen, an increase from none who believed so the previous month.

- 29.6% of survey respondents believe demand for leases and loans to fund capital expenditures (capex) will increase over the next four months, down from 40.9% in August. 59.3% believe demand will “remain the same” during the same four-month time period, unchanged from the previous month. 11.1% believe demand will decline, an increase from none who believed so in August.

- 25.9% of executives expect more access to capital to fund equipment acquisitions over the next four months, down from 31.8% in August. 70.4% of survey respondents indicate they expect the “same” access to capital to fund business, up from 68.2% in August. 3.7% expect “less” access to capital, up from none the previous month.

- When asked, 37.0% of the executives report they expect to hire more employees over the next four months, a slight increase from 36.4% in August. 59.3% expect no change in headcount over the next four months, down from 63.6% last month. 3.7% expect to hire fewer employees, up from none in August.

- None of the leadership evaluate the current U.S. economy as “excellent,” a decrease from 4.5% last month. 96.3% of the leadership evaluate the current U.S. economy as “fair,” up from 95.5% in August. 3.7% rate it as “poor,” an increase from none the previous month.

- 18.5% of the survey respondents believe that U.S. economic conditions will get “better” over the next six months, a decrease from 27.3% who believed so in August. 74.1% of survey respondents indicate they believe the U.S. economy will “stay the same” over the next six months, up from 68.2% in August. 7.4% believe economic conditions in the U.S. will worsen over the next six months, an increase from 4.5% who believed so last month.

- In September, 51.9% of respondents indicate they believe their company will increase spending on business development activities during the next six months, a decrease from 54.5% in August. 44.4% believe there will be “no change” in business development spending, a decrease from 45.5% last month. 3.7% believe there will be a decrease in spending, an increase from none last month.

Survey Demographics

Market Segment:

- Bank: 80.8%

- Captive: 3.8%

- Financial Services: 3.8%

- Independent: 11.5%

- Other: 0.0%

Market Segments Based on Transaction Size of New Business Volume

- Large-Ticket (New Business Volume Avg. Transaction Size Over $5 Million): 15.4%

- Middle-Ticket (New Business Volume Avg. Transaction Size of $250,000 – $5 Million): 53.8%

- Small-Ticket (New Business Volume Avg. Transaction Size of $25,000 – $249,999): 30.8%

- Micro-Ticket (New Business Volume Avg. Transaction Less Than $25,000): 0.0%

Organization Size (Based on Annual New Business Volume for Fiscal Year 2010):

- Under $50 Million: 7.7%

- $50 Million – $250 Million: 7.7%

- $250 Million – $1 Billion: 30.8%

- Over $1 Billion: 53.8%

September 2015 Survey Comments from Industry Executive Leadership

Depending on the market segment they represent, executives have differing points of view on the current and future outlook for the industry.

Independent, Small Ticket

“We are still bullish as we head into the fourth quarter. Demand continues to be strong and in spite of the recent fluctuations of the stock market, our customers are continuing with business expansion projects and replacement of equipment.” Valerie Hayes Jester, President, Brandywine Capital Associates, Inc.

Bank, Middle Ticket

“Replacement equipment financing and equipment debt consolidation continue, but expansionary plans are becoming less robust. The full effect of international economic problems are the largest inhibitor to growth in the U.S.” Harry Kaplun, President, Specialty Finance, Frost Bank

Bank, Middle Ticket

“[I am] concerned about the energy sector and the decline in energy capex. About 20% of our business is centered in energy, and the decline in oil prices has put several projects on hold.” Elaine Temple, President, BancorpSouth Equipment Finance

Back to Top