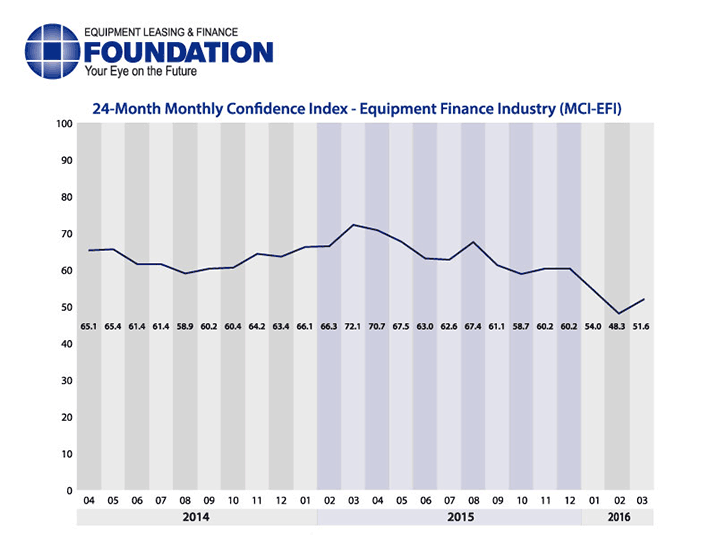

The Equipment Leasing & Finance Foundation (the Foundation) releases the March 2016 Monthly Confidence Index for the Equipment Finance Industry (MCI-EFI) today. Designed to collect leadership data, the index reports a qualitative assessment of both the prevailing business conditions and expectations for the future as reported by key executives from the $1 trillion equipment finance sector. Overall, confidence in the equipment finance market is 51.6, an increase from the February index of 48.3.

When asked about the outlook for the future, MCI-EFI survey respondent Paul Menzel, President & CEO, Financial Pacific Leasing, LLC, said, “I believe the fundamentals of the U.S. economy are strong. Low energy costs, which are a net positive for small businesses and consumers, provide a hedge against recession and/or inflation. The presidential election rancor and uncertainty will keep a damper on any substantial growth or improvement in the economy for 2016.”

March 2016 Survey Results

The overall MCI-EFI is 51.6, an increase from the February index of 48.3.

- When asked to assess their business conditions over the next four months, 3.2% of executives responding said they believe business conditions will improve over the next four months, unchanged from February. 77.4% of respondents believe business conditions will remain the same over the next four months, an increase from 71.0% in February. 19.4% believe business conditions will worsen, a decrease from 25.8% the previous month.

- 9.7% of survey respondents believe demand for leases and loans to fund capital expenditures (capex) will increase over the next four months, an increase from 3.2% in February. 74.2% believe demand will “remain the same” during the same four-month time period, up from 61.3% the previous month. 16.1% believe demand will decline, a decrease from 35.5% who believed so in February.

- 16.1% of executives expect more access to capital to fund equipment acquisitions over the next four months, unchanged from February. 77.4% of survey respondents indicate they expect the “same” access to capital to fund business, an increase from 71.0% the previous month. 6.5% expect “less” access to capital, a decrease from 12.9% last month.

- When asked, 32.3% of the executives report they expect to hire more employees over the next four months, an increase from 29.0% in February. 61.3% expect no change in headcount over the next four months, a decrease from 64.5 last month. 6.5% expect to hire fewer employees, unchanged from February.

- None of the leadership evaluate the current U.S. economy as “excellent,” unchanged from last month. 100% of the leadership evaluate the current U.S. economy as “fair,” up from 96.8% in February. None rate it as “poor,” down from 3.2% the previous month.

- None of the survey respondents believe that U.S. economic conditions will get “better” over the next six months, a decrease from 6.5% who believed so in February. 77.4% of survey respondents indicate they believe the U.S. economy will “stay the same” over the next six months, an increase from 67.7% the previous month. 22.6% believe economic conditions in the U.S. will worsen over the next six months, a decrease from 25.8% who believed so last month.

- In March, 38.7% of respondents indicate they believe their company will increase spending on business development activities during the next six months, a decrease from 41.9% in February. 48.4% believe there will be “no change” in business development spending, unchanged from the previous month. 12.9% believe there will be a decrease in spending, an increase from 9.7% who believed so last month.

Survey Demographics

Market Segment:

- Bank: 64.5%

- Captive: 6.5%

- Financial Services: 3.2%

- Independent: 25.8%

- Other: 0.0%

Market Segments Based on Transaction Size of New Business Volume

- Large-Ticket (New Business Volume Avg. Transaction Size Over $5 Million): 16.1%

- Middle-Ticket (New Business Volume Avg. Transaction Size of $250,000 – $5 Million): 41.9%

- Small-Ticket (New Business Volume Avg. Transaction Size of $25,000 – $249,999): 41.9%

- Micro-Ticket (New Business Volume Avg. Transaction Less Than $25,000): 0.0%

Organization Size (Based on Annual New Business Volume for Fiscal Year 2010):

- Under $50 Million: 6.5%

- $50 Million – $250 Million: 19.4%

- $250 Million – $1 Billion: 29.0%

- Over $1 Billion: 45.2%

March 2016 Survey Comments from Industry Executive Leadership

Depending on the market segment they represent, executives have differing points of view on the current and future outlook for the industry.

Independent, Small Ticket

“Application volume and approvals remain strong but closing them has been difficult. We attribute this to competitive factors from within our industry and from the alternative finance industry. There still seems to be a level of uncertainty in the small business market as well.” David T. Schaefer, CEO, Mintaka Financial, LLC

Bank, Middle Ticket

“There are pockets of opportunity in both types of equipment and specific industries. That said, there are an increasing number of industries that are hitting a reset button with regard to growth and capital spending.” Harry Kaplun, President, Specialty Finance, Frost Bank

Independent, Middle Ticket

“Continued growth in new business opportunities, tempered with some slowdown in the Class 8 truck market, and an increase in repossessions cause some concern. Is this an early warning signal?” William H. Besgen, Vice Chairman Board of Directors, Hitachi Capital America Corp.

Bank, Large Ticket

“Outside of oil there still appears to be a good demand for new equipment in the markets we serve. Talent development is a key concern for the future of the industry.” Thomas Partridge, President, Fifth Third Equipment Finance

Back to Top