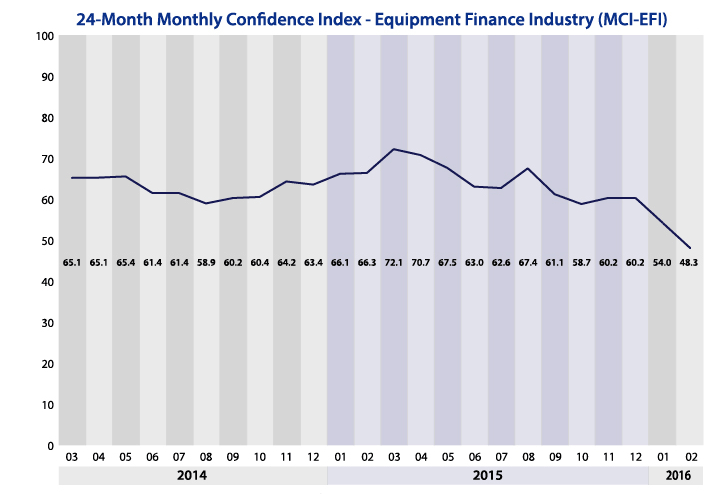

The Equipment Leasing & Finance Foundation (the Foundation) releases the February 2016 Monthly Confidence Index for the Equipment Finance Industry (MCI-EFI) today. Designed to collect leadership data, the index reports a qualitative assessment of both the prevailing business conditions and expectations for the future as reported by key executives from the $1 trillion equipment finance sector. Overall, confidence in the equipment finance market is 48.3, with uncertainty on various fronts cited for the decrease from the January index of 54.0.

When asked about the outlook for the future, MCI-EFI survey respondent Harry Kaplun, President, Specialty Finance, Frost Bank, said, “Uncertainty on the international front and with energy markets is creating capital expenditure restraint. More clarity should emerge in the second half of 2016.”

February 2016 Survey Results

The overall MCI-EFI is 48.3, a decrease from the January index of 54.0.

- When asked to assess their business conditions over the next four months, 3.2% of executives responding said they believe business conditions will improve over the next four months, a decrease from 10.7% in January. 71.0% of respondents believe business conditions will remain the same over the next four months, a decrease from 78.6% in January. 25.8% believe business conditions will worsen, an increase from 10.7% the previous month.

- 3.2% of survey respondents believe demand for leases and loans to fund capital expenditures (capex) will increase over the next four months, a decrease from 10.7% in January. 61.3% believe demand will “remain the same” during the same four-month time period, down from 71.4% the previous month. 35.5% believe demand will decline, an increase from 17.9% who believed so in January.

- 16.1% of executives expect more access to capital to fund equipment acquisitions over the next four months, a decrease from 17.9% in January. 71.0% of survey respondents indicate they expect the “same” access to capital to fund business, a decrease from 75.0% the previous month. 12.9% expect “less” access to capital, an increase from 7.1% last month.

- When asked, 29.0% of the executives report they expect to hire more employees over the next four months, a decrease from 32.1% in January. 64.5% expect no change in headcount over the next four months, unchanged from last month. 6.5% expect to hire fewer employees, up from 3.6% in January.

- None of the leadership evaluate the current U.S. economy as “excellent,” a decrease from 3.6% last month. 96.8% of the leadership evaluate the current U.S. economy as “fair,” up from 92.9% in January. 3.2% rate it as “poor,” relatively unchanged from the previous month.

- 6.5% of the survey respondents believe that U.S. economic conditions will get “better” over the next six months, an increase from 3.6% who believed so in January. 67.7% of survey respondents indicate they believe the U.S. economy will “stay the same” over the next six months, a decrease from 75.0% the previous month. 25.8% believe economic conditions in the U.S. will worsen over the next six months, an increase from 21.4% who believed so last month.

- In February, 41.9% of respondents indicate they believe their company will increase spending on business development activities during the next six months, an increase from 35.7% in January. 48.4% believe there will be “no change” in business development spending, a decrease from 64.3% the previous month. 9.7% believe there will be a decrease in spending, an increase from none who believed so last month.

Survey Demographics

Market Segment:

- Bank: 69.0%

- Captive: 3.4%

- Financial Services: 3.4%

- Independent: 17.2%

- Other: 6.9%

Market Segments Based on Transaction Size of New Business Volume

- Large-Ticket (New Business Volume Avg. Transaction Size Over $5 Million): 17.2%

- Middle-Ticket (New Business Volume Avg. Transaction Size of $250,000 – $5 Million): 51.7%

- Small-Ticket (New Business Volume Avg. Transaction Size of $25,000 – $249,999): 31.0%

- Micro-Ticket (New Business Volume Avg. Transaction Less Than $25,000): 0.0%

Organization Size (Based on Annual New Business Volume for Fiscal Year 2010):

- Under $50 Million: 0.0%

- $50 Million – $250 Million: 13.8%

- $250 Million – $1 Billion: 34.5%

- Over $1 Billion: 51.7%

February 2016 Survey Comments from Industry Executive Leadership

Depending on the market segment they represent, executives have differing points of view on the current and future outlook for the industry.

Bank, Small Ticket

“A flat domestic economy, muffled by presidential election uncertainty, will subdue growth in our industry for 2016.” Paul Menzel, President & CEO, Financial Pacific Leasing, LLC

Independent, Small Ticket

“I think we are beginning to see a bit of a pullback in the small business space. Even though application volume is steady, we are seeing fewer deals being closed. Seems like uncertainty about the economy is creeping in.” David T. Schaefer, CEO, Mintaka Financial, LLC

Independent, Middle Ticket

“Targeted business volumes seem to be holding in all of our business segments, but the big question is what will the impact of lower oil prices and the apparent negative sentiment created in the energy and banking community do to slow the rest of the economy?” William H. Besgen, Vice Chairman Board of Directors, Hitachi Capital America Corp.

Bank, Large Ticket

“Capital is still readily available. Banks and lending institutions are trying to get money out the door.” Thomas Partridge, President, Fifth Third Equipment Finance

Back to Top