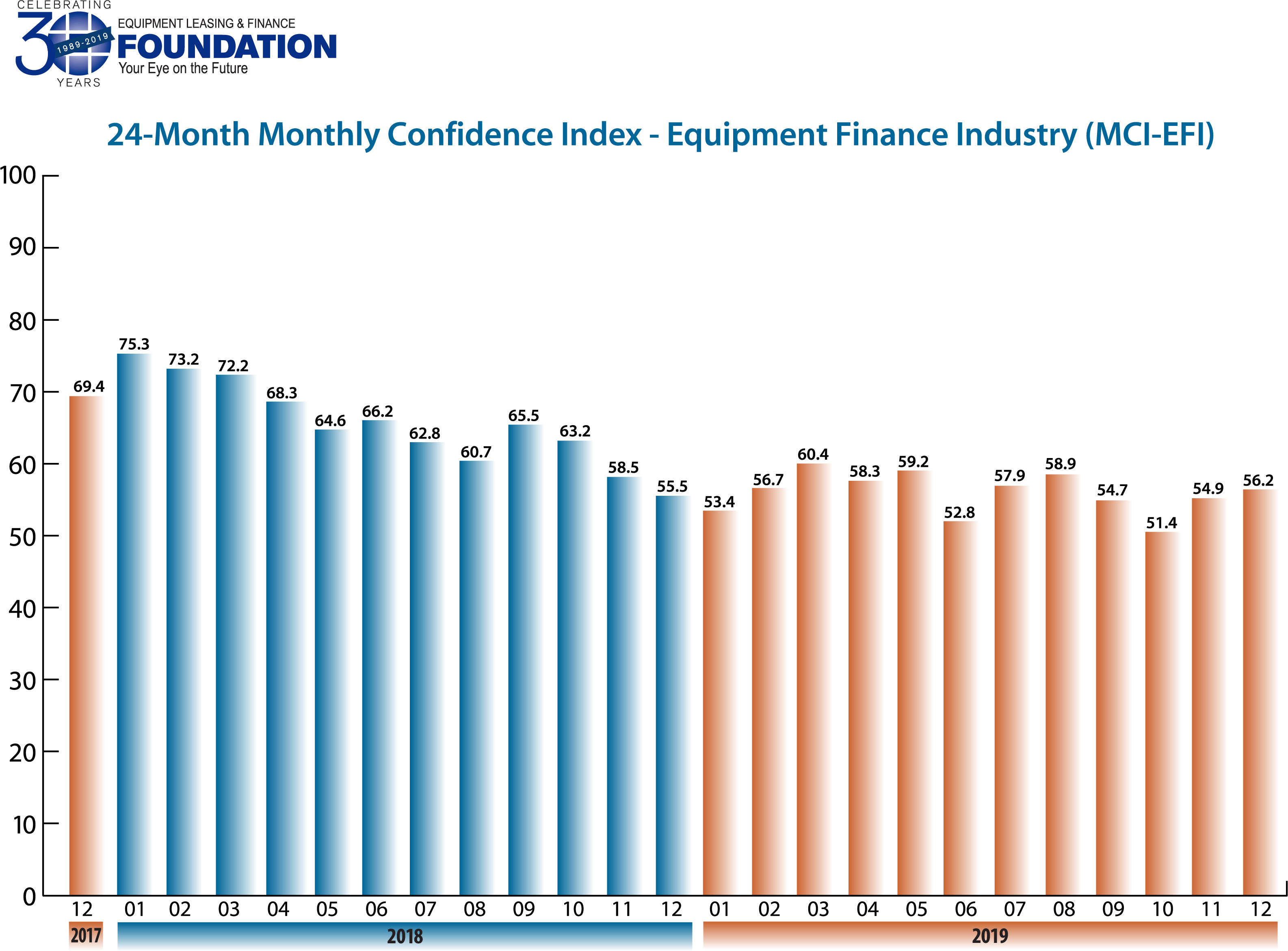

The Equipment Leasing & Finance Foundation (the Foundation) releases the December 2019 Monthly Confidence Index for the Equipment Finance Industry (MCI-EFI) today. Designed to collect leadership data, the index reports a qualitative assessment of both the prevailing business conditions and expectations for the future as reported by key executives from the $900 billion equipment finance sector. Overall, confidence in the equipment finance market is 56.2, an increase from the November index of 54.9.

When asked about the outlook for the future, MCI-EFI survey respondent Valerie Jester, President, Brandywine Capital Associates, Inc., said, “We are experiencing a strong finish to the year and the fourth quarter. Given all the distractions of the national political stage I am a bit surprised. The tariffs that were imposed earlier in the year are having their effect on certain industries, but we continue to see good investment in equipment with the predominance of our customer base. I believe many have learned to tune out the ‘noise’ and focus on the necessities to compete in today’s markets. Waiting to make certain equipment investments is just not optional if you want to stay in the game.”

December 2019 Survey Results

The overall MCI-EFI is 56.2, an increase from 54.9 in November.

- When asked to assess their business conditions over the next four months, 10.3% of executives responding said they believe business conditions will improve over the next four months, down from 13.3% in November. 82.8% of respondents believe business conditions will remain the same over the next four months, an increase from 73.3% the previous month. 6.9% believe business conditions will worsen, down from 13.3% in November.

- 10% of the survey respondents believe demand for leases and loans to fund capital expenditures (capex) will increase over the next four months, a decrease from 13.3% in November. 76.7% believe demand will “remain the same” during the same four-month time period, an increase from 63.3% the previous month. 13.3% believe demand will decline, down from 23.3% in November.

- 20% of the respondents expect more access to capital to fund equipment acquisitions over the next four months, 80% of executives indicate they expect the “same” access to capital to fund business, and none expect “less” access to capital, all unchanged from November.

- When asked, 30% of the executives report they expect to hire more employees over the next four months, an increase from 26.7% in November. 63.3% expect no change in headcount over the next four months, a decrease from 73.3% last month. 6.7% expect to hire fewer employees, up from none the previous month.

- 23.3% of the leadership evaluate the current U.S. economy as “excellent,” up from 16.7% the previous month. 76.7% of the leadership evaluate the current U.S. economy as “fair,” down from 83.3% in November. None evaluate it as “poor,” unchanged from last month.

- 13.3% of the survey respondents believe that U.S. economic conditions will get “better” over the next six months, up from 10% in November. 80% of survey respondents indicate they believe the U.S. economy will “stay the same” over the next six months, an increase from 76.7% the previous month. 6.7% believe economic conditions in the U.S. will worsen over the next six months, a decrease from 13.3% in November.

- In December, 23.3% of respondents indicate they believe their company will increase spending on business development activities during the next six months, a decrease from 30% last month. 73.3% believe there will be “no change” in business development spending, an increase from 63.3% in November. 3.3% believe there will be a decrease in spending, down from 6.7% last month.

Survey Demographics

Market Segment

- Bank 60%

- Captive 10%

- Financial Services 3.3%

- Independent 23.3%

- Other 3.3%

Market Segments Based on Transaction Size of New Business Volume

- Large-Ticket (New Business Volume Avg. Transaction Size Over $5 Million) 23.3%

- Middle-Ticket (New Business Volume Avg. Transaction Size of $250,000 – $5 Million) 53.3%

- Small-Ticket (New Business Volume Avg. Transaction Size of $25,000 – $249,999) 23.3%

- Micro-Ticket (New Business Volume Avg. Transaction Less Than $25,000) 0.00%

Organization Size

- Under $50 Million 6.7%

- $50 Million – $250 Million 16.7%

- $250 Million – $1 Billion 23.3%

- Over $1 Billion 53.3%

December 2019 Survey Comments from Industry Executive Leadership

Independent, Small Ticket

“We’re more hopeful than optimistic that there is pent-up small business capital equipment demand that will release and spur increased financing volume. We wonder whether the trucking recession is the canary in a coalmine for future problems, or an isolated sector problem.” Quentin Cote, CLFP, President, Mintaka Financial, LLC,

Bank, Small Ticket

“Our volume, credit quality and portfolio performance have all remained strong. Economic indicators are positive. Moving into an election year and the uncertainty that comes with it may cause stagnation.” David Normandin, CLFP, President and CEO, Wintrust Specialty Finance

Bank, Middle Ticket

“Demand for financing within our core commercial & industrial loan business remains steady, and the pipeline is strong into the beginning of 2020 indicating continued pent-up demand for capital expenditures. Money costs remain at all-time lows, which may continue to fuel growth. Unemployment numbers continue to decline. Admittedly there is uncertainty in some sectors such as rail, but these seem to be cyclical in nature and focus primarily around energy. We do anticipate growth in the plastics sector to offset some of this.” Frank Campagna, Business Line Manager, M&T Commercial Equipment Finance

Back to Top