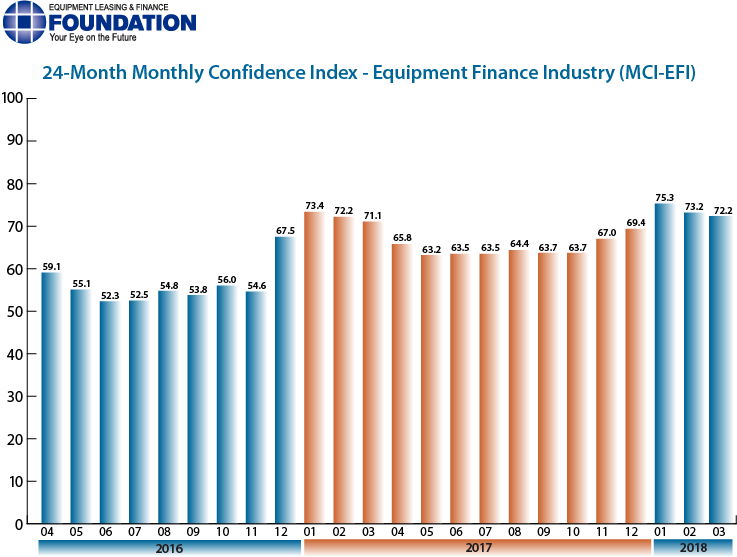

The Equipment Leasing & Finance Foundation (the Foundation) releases the March 2018 Monthly Confidence Index for the Equipment Finance Industry (MCI-EFI) today. Designed to collect leadership data, the index reports a qualitative assessment of both the prevailing business conditions and expectations for the future as reported by key executives from the $1 trillion equipment finance sector. Overall, confidence in the equipment finance market is 72.2 in March, easing slightly from 73.2 in February.

When asked about the outlook for the future, MCI-EFI survey respondent Anthony Cracchiolo, President and CEO, U.S. Bank Equipment Finance, said, “We are seeing growth in capex spending across a broad segment of the economy. While some areas are expanding more quickly than others, all are moving in a positive direction. Businesses are more positive then we have seen in over a decade and activity is picking up momentum. The equipment finance industry is healthy and poised to support the expanding economy.”

March 2018 Survey Results

The overall MCI-EFI is 72.2 in March, easing from 73.2 in February.

- When asked to assess their business conditions over the next four months, 54.8% of executives responding said they believe business conditions will improve over the next four months, an increase from 46.4% in February. 45.2% of respondents believe business conditions will remain the same over the next four months, a decrease from 53.6% the previous month. None believe business conditions will worsen, unchanged from the previous month.

- 67.7% of survey respondents believe demand for leases and loans to fund capital expenditures (capex) will increase over the next four months, unchanged from February. 32.3% believe demand will “remain the same” during the same four-month time period, relatively unchanged from 32.1% the previous month. None believe demand will decline, also unchanged from February.

- 22.6% of the respondents expect more access to capital to fund equipment acquisitions over the next four months, down from 28.6% in February. 74.2% of executives indicate they expect the “same” access to capital to fund business, an increase from 67.9% last month. 3.2% expect “less” access to capital, down slightly from 3.6% last month.

- When asked, 41.9% of the executives report they expect to hire more employees over the next four months, a decrease from 42.9% in February. 51.6% expect no change in headcount over the next four months, a decrease from 53.6% last month. 6.5% expect to hire fewer employees, up from 3.6% in February.

- 29.0% of the leadership evaluate the current U.S. economy as “excellent,” up from 25.0% last month. 71.0% of the leadership evaluate the current U.S. economy as “fair,” down from 75.0% in February. None evaluate it as “poor,” unchanged from last month.

- 45.2% of the survey respondents believe that U.S. economic conditions will get “better” over the next six months, a decrease from 60.7% in February. 51.6% of survey respondents indicate they believe the U.S. economy will “stay the same” over the next six months, an increase from 35.7% the previous month. 3.2% believe economic conditions in the U.S. will worsen over the next six months, a slight decrease from 3.6% in February.

- In March, 51.6% of respondents indicate they believe their company will increase spending on business development activities during the next six months, a decrease from 53.6% in February. 45.2% believe there will be “no change” in business development spending, a decrease from 46.4% the previous month. 3.2% believe there will be a decrease in spending, an increase from none who believed so last month.

Survey Demographics

Market Segment

- Bank 63.33%

- Captive 13.33%

- Financial Services 3.33%

- Independent 20.00%

- Other (please specify) 0.00%

Market Segments Based on Transaction Size of New Business Volume

- Large-Ticket (New Business Volume Avg. Transaction Size Over $5 Million) 20.00%

- Middle-Ticket (New Business Volume Avg. Transaction Size of $250,000 – $5 Million) 50.00%

- Small-Ticket (New Business Volume Avg. Transaction Size of $25,000 – $249,999) 30.00%

- Micro-Ticket (New Business Volume Avg. Transaction Less Than $25,000) 0.00%

Organization Size

- Under $50 Million 6.67%

- $50 Million – $250 Million 13.33%

- $250 Million – $1 Billion 20.00%

- Over $1 Billion 60.00%

March 2018 Survey Comments from Industry Executive Leadership

Independent, Small Ticket

“In spite of the gyrations of the stock market, our customers seem poised to grow their businesses. We have experienced more demand for expansion projects in the last few months than in all of 2017. That type of optimism fuels a strong demand for financing products. Tax reform and interest rates that continue to be favorable, in spite of increases recently, should create strong growth for 2018.” Valerie Hayes Jester, President, Brandywine Capital Associates

Bank, Small Ticket

“Tax reform, market optimism, and a 17-year low unemployment rate are all reasons that I am confident in the economy and our specific segment of the market. While rising interest rates are good for our business in the long term, in the short term it is a challenge to keep pace in the market given robust competition.” David Normandin, CLFP, Managing Director, Commercial Finance Group, Hanmi Bank

Bank, Middle Ticket

“We are still experiencing customers digesting the tax reform changes and how this will impact their decisions on buy vs lease. In some cases, this has delayed purchasing decisions or project start dates.” Michael Romanowski, President, Farm Credit Leasing Services Corporation

Back to Top